America's Financial System

Understanding America's financial system is essential for anyone who wants to navigate the modern economy with confidence and clarity.

The Core Structure of the U.S. Financial System

The American financial system operates as a complex but remarkably coordinated network of institutions, markets, and regulations designed to move capital from savers to borrowers. At its foundation, the system balances private enterprise with public oversight, ensuring that credit, payments, and investment flow smoothly through the economy. This structure includes commercial banks, investment banks, insurance companies, pension funds, and a dense web of payment systems that make everyday transactions possible.

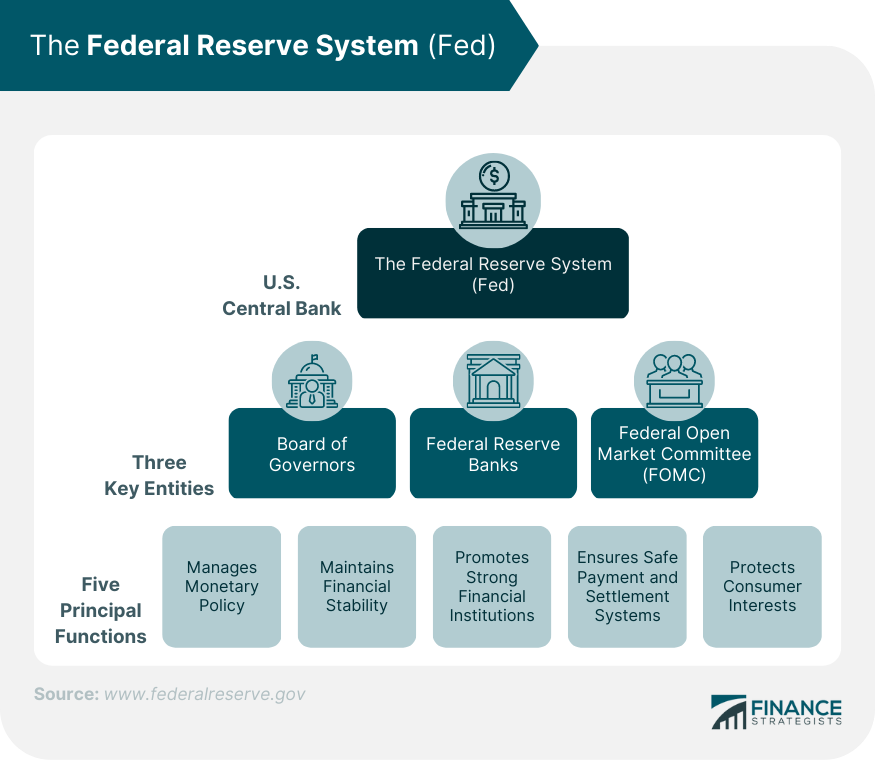

Central to this architecture is the role of the Federal Reserve, which sets monetary policy, supervises key banks, and acts as a lender of last resort. By managing interest rates and the money supply, the Fed influences everything from mortgage rates to business investment. Complementing this are prudential regulators like the Office of the Comptroller of the Currency and state-level authorities, each with specific mandates to maintain stability, protect consumers, and prevent reckless risk-taking.

Commercial Banking and the Flow of Everyday Finance

For most people, the most visible part of America's financial system is the commercial banking sector, where checking and savings accounts, debit cards, and consumer loans live. Banks gather deposits from households and small businesses, then channel those funds into mortgages, credit cards, and small-business lines of credit, effectively transforming short-term deposits into longer-term loans. This process, known as financial intermediation, is what makes it possible for families to buy homes and entrepreneurs to launch or expand companies.

Deposit insurance, primarily through the Federal Deposit Insurance Corporation, helps maintain public trust by guaranteeing that ordinary depositors can access their money even if a bank runs into trouble. At the same time, strict capital and liquidity requirements aim to ensure that banks remain resilient during economic downturns. Together, these safeguards help prevent the kind of widespread bank runs that turned local missteps into systemic crises.

Capital Markets and Long-Term Investment

Beyond day-to-day banking, America's financial system relies heavily on deep and liquid capital markets, where stocks, bonds, and other securities are bought and sold. These markets allow companies to raise large amounts of capital for innovation and expansion, giving investors a chance to share in the growth of the economy. Through initial public offerings, secondary trading, and bond issuances, capital markets price risk, set the cost of capital, and allocate resources toward the most promising opportunities.

- Equity markets provide ownership stakes in public companies, enabling broad participation in corporate profits.

- Debt markets offer government and corporate bonds that serve as relatively stable investments and benchmarks for interest rates.

- Together, these markets underpin everything from retirement savings to the financing of cutting-edge technology.

Regulatory bodies such as the Securities and Exchange Commission work to promote transparency, prevent fraud, and ensure that investors have access to accurate information. While these markets can be volatile, their overall design encourages long-term capital formation and supports the dynamic, innovation-driven character of the U.S. economy.

The Federal Reserve, Monetary Policy, and Financial Stability

The Federal Reserve stands at the center of monetary policy in the United States, using tools such as the federal funds rate, open market operations, and forward guidance to steer the economy toward its dual mandate of maximum employment and stable prices. By influencing short-term interest rates, the Fed affects borrowing costs across the entire financial system, from the interest consumers pay on credit cards to the rates businesses face when issuing bonds.

In times of stress, the Fed can act as a market maker of last resort, providing liquidity to banks, broker-dealers, and other critical institutions to keep financial markets functioning. This role became especially prominent during the global financial crisis and again during the pandemic, when rapid interventions helped prevent a complete freeze in credit markets. At the same time, ongoing supervision and stress testing aim to strengthen the largest institutions so that shocks are absorbed without cascading failures.

Payments, Digital Finance, and the Evolving Landscape

Modern America's financial system is also defined by its payments infrastructure, which has evolved from paper checks to instant digital transfers, mobile wallets, and real-time payment platforms. Faster payment systems are steadily reducing the time between sending and receiving money, improving efficiency for consumers and businesses alike. At the same time, new technologies, including blockchain, digital currencies, and open banking initiatives, are reshaping how people interact with money and credit.

These innovations bring both opportunity and challenge, raising important questions around privacy, cybersecurity, and consumer protection. Regulators and industry leaders are working to update rules so that new technologies can thrive without compromising safety or fairness. As fintech companies partner with or compete with traditional banks, the overall system is becoming more interconnected, data-driven, and responsive to customer expectations.

Consumer Protection, Regulation, and Public Trust

A durable financial system depends on public confidence that institutions will treat customers fairly and that there are clear rules in place to prevent abuse. Consumer protection laws, enforced by agencies such as the Consumer Financial Protection Bureau, set standards for transparency in lending, credit reporting, and fee structures. These rules aim to ensure that products are understandable and that consumers are not subjected to predatory or deceptive practices.

Ongoing debates about regulation often center on finding the right balance between fostering innovation and maintaining safeguards. Strong oversight helps curb excessive risk-taking, but it must be designed in a way that does not choke off credit or burden responsible institutions. When people trust that their money is safe and that the system is fair, they are more likely to save, invest, and participate fully in economic life.

In the end, America's financial system is both a reflection of the country's broader economic values and a powerful tool that shapes everyday life. From the neighborhood bank to global capital markets and cutting-edge digital payments, each piece contributes to how resources are allocated, how risk is managed, and how opportunities are created. Understanding this system empowers individuals and businesses to make smarter decisions, adapt to change, and contribute to a more resilient and inclusive economic future.

The Federal Reserve: Inside the Most Powerful Financial Institution on Earth | FD Finance

... about the decisions that helped lead the global financial system to the brink of collapse in 2008. And why we might be headed ...